Biden's student loan relief plan is currently on hold. Here's what borrowers should be aware of.

- Over 8 million individuals have enrolled in SAVE, the innovative income-based repayment program.

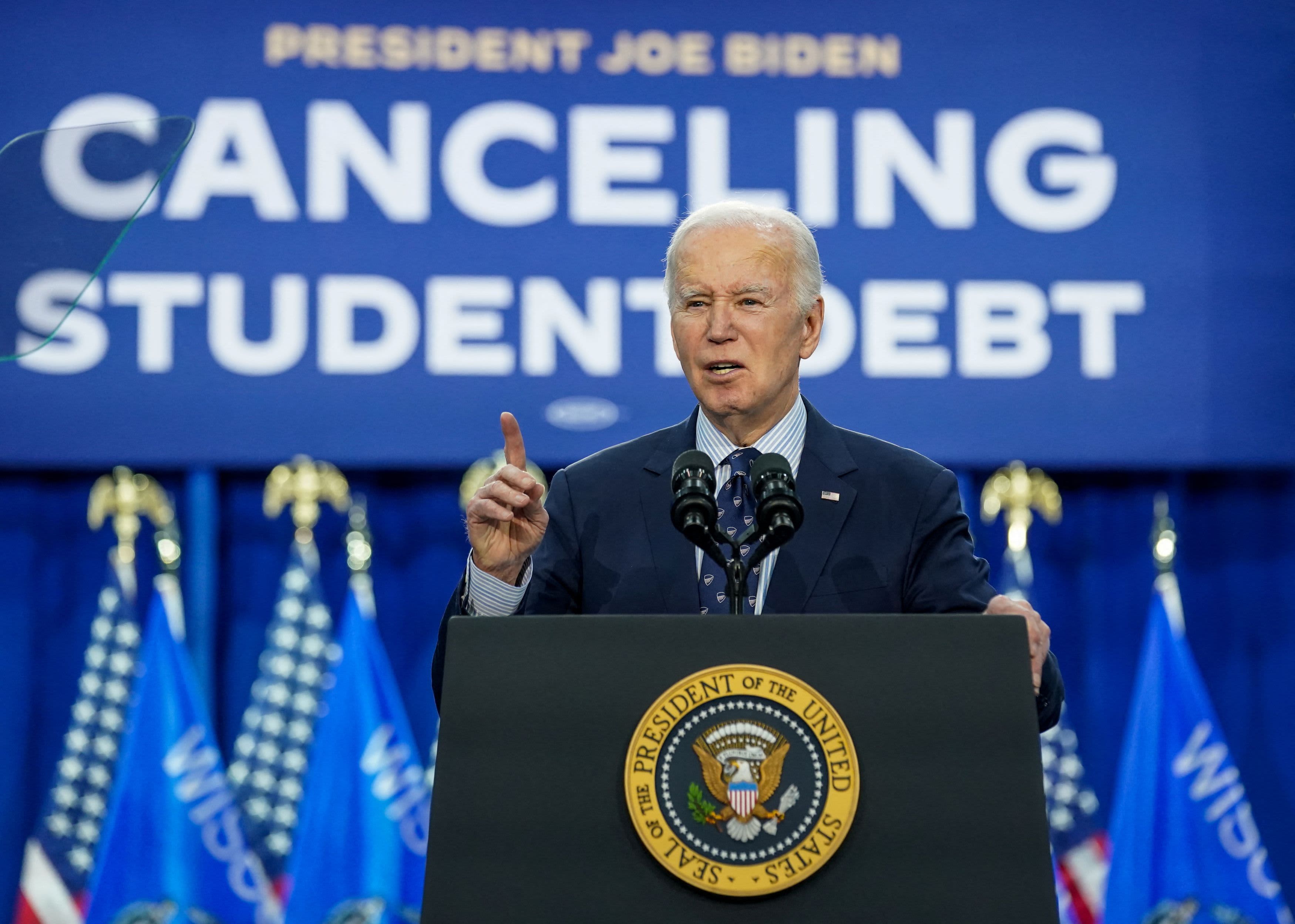

- The Biden administration's relief plan for student loan borrowers was halted by two federal judges just days before millions of borrowers were expected to see their monthly bill drop by half or more.

- Borrowers can remain in the SAVE plan, but it's important for them to be aware of certain details.

Cody Gude eagerly awaited July to arrive, as his monthly student loan payment would decrease from $200 to $100.

He no longer needed to deliver groceries on top of his work as a social media consultant due to the lower payment.

"I could breathe," said the 35-year-old resident of Tampa, Florida.

The Biden administration's new repayment plan for student loans was temporarily halted by two federal judges in Kansas and Missouri.

The preliminary injunctions issued by the U.S. Department of Justice are expected to be appealed, leaving millions of student loan borrowers feeling disappointed and angry as they wait for the relief they had hoped for in just a matter of days.

Inflation continues to disrupt retirement plans for older voters. Candidates who promise to safeguard Social Security are in high demand among this demographic. Workers in certain industries typically have higher 401(k) balances.

There's a great deal of confusion as well.

Nelnet, Gude's student loan servicer, has already adjusted his monthly bill to reflect the reduced amount. (Under SAVE, many borrowers pay only 5% of their discretionary income towards their debt each month instead of the previous 10% requirement, and millions of borrowers have a $0 monthly payment.)

"Am I going to receive that payment, or will I receive a letter stating, 'Just kidding,'" Gude said. "No one knows."

Here's what we know so far.

Why is the SAVE plan causing drama?

The SAVE plan, which was introduced by President Joe Biden last summer, is described as the most affordable student loan plan available. Approximately 8 million borrowers have enrolled in the new income-driven repayment plan, according to the White House.

SAVE is a new plan that replaces the U.S. Department of Education's former REPAYE option, under which borrowers pay a portion of their discretionary income each month and receive loan forgiveness after a set period, typically 20 years or 25 years.

The current controversy surrounding the SAVE plan arises from its generous terms.

Borrowers under REPAYE now need to pay only 5% of their discretionary income monthly towards their undergraduate student debt, instead of the previous 10%.

Individuals earning less than $15 per hour receive a monthly bill of $0, while borrowers with smaller balances are eligible for loan forgiveness in as little as 10 years.

Mark Kantrowitz, a higher education expert, stated that the SAVE plan is extremely generous to borrowers, almost like a grant post-factum.

Although some features of the SAVE plan were already available to borrowers, the plan was not fully scheduled to take effect until July 1 due to the timeline of regulatory changes.

Under the plan, $4.8 billion in debt relief was provided to 360,000 borrowers by the Education Department by mid-April.

What did the judges decide?

Federal judges have reacted to lawsuits against the SAVE plan, which was filed earlier this year by Republican-led states such as Florida, Arkansas, and Missouri.

The Biden administration's attempt to forgive student debt through SAVE was met with opposition from the states, who claimed it was an overreach of authority and a roundabout way to achieve the same goal after the Supreme Court blocked the plan last year.

Daniel Crabtree, a federal judge in Kansas, refused to reverse the SAVE plan's features that were already in effect because the plaintiffs failed to prove that those provisions caused irreparable harm, as they had filed the lawsuit after the defendants had already implemented those aspects of the SAVE Plan.

Crabtree halted the Education Department from implementing the SAVE provision that lowers borrowers' monthly payments in July. He argued that the REPAYE plan, which SAVE replaced, cost an estimated $15.4 billion, while the SAVE plan is expected to cost $475 billion over the next decade.

"The difference between $475 billion and $15.4 billion is so significant that it changes the authority of the agency. As a result, the court determines that the SAVE Plan represents a massive and transformative expansion of regulatory authority without proper authorization from Congress."

In Missouri, Judge John Ross halted the Biden administration's plan to forgive additional student debt under the SAVE program until he made a ruling on the case. Ross concurred with the states that the relief plan would likely decrease the fees the government pays to the Missouri Higher Education Loan Authority (Mohela) for servicing its federal student loans.

What is the estimated duration of this legal case?

Scott Buchanan, the executive director of the Student Loan Servicing Alliance, a trade group for federal student loan servicers, said, "I suspect months have passed since the election."

Buchanan believes that the cases will not be taken up by the Supreme Court until the October term, resulting in a much later ruling.

In the meantime, what do borrowers do?

Although the judges did not pause the provision that protects a larger portion of borrowers' income from their payment calculation, borrowers can still remain enrolled in the SAVE plan and continue to benefit from lower bills.

If your servicer updated your monthly bill to what it was going to be before the preliminary injunctions, your required payment should soon revert back to its June level, experts advise.

"Kantrowitz stated that the court's ruling is not retroactive, meaning borrowers do not need to worry about the courts taking back the loan forgiveness they have already received."

Investing

You might also like

- In 2025, there will be a significant alteration to inherited IRAs, according to an advisor. Here's how to avoid penalties.

- An expert suggests that now is the 'optimal moment' to reevaluate your retirement savings. Here are some tips to help you begin.

- A human rights expert explains why wealth accumulation is increasing at an accelerated rate during the era of the billionaire.

- Social media influencers are here to stay, regardless of what happens with TikTok. Here's how to vet money advice from them.

- This tax season, investors may be eligible for free tax filing.